Coming out of the "storm"

Although hit by a global pandemic that caused shop owners to rethink how to run their business, many fabricators express signs of optimism for 2021

2020 was an unprecedented year. Last January, undoubtedly, no one would have predicted that the COVID-19 global pandemic would strike with such force and stop “normal” life for so many people. Overall, North American fabricators have stayed afloat – navigating many obstacles and uncertainties. And while what the near future has in store is still unclear, Stone World’s recent Fabricator Forecast, which is conducted by Clear Seas Research Department at BNP Media (Stone World’s parent company), shows that more than two-thirds of fabricators polled are hopeful that business will fare well this year.

Predictions for 2021

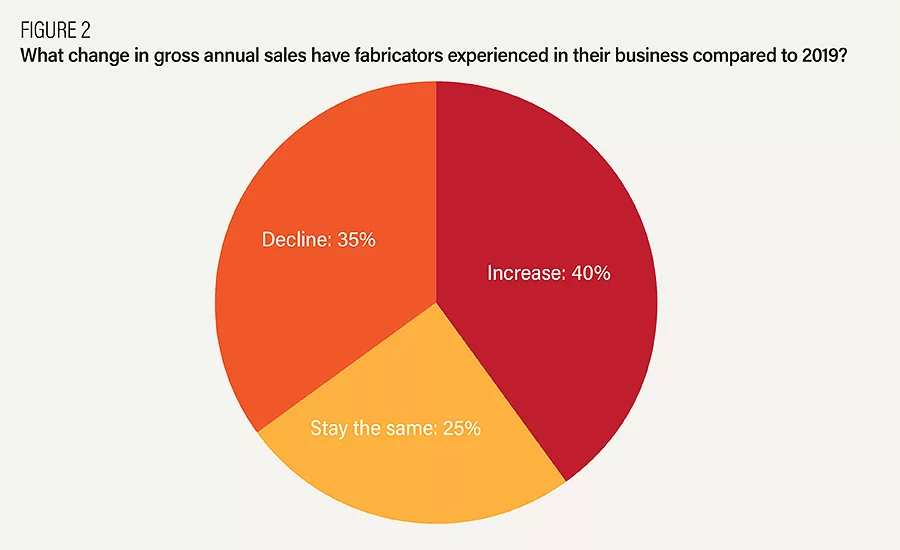

The survey indicates that two-in-five respondents (40%) have seen an increase in their companies’ gross annual sales over the last year, by an average of 32%, while more than one-third (35%) of respondents report that their companies’ gross annual sales have declined over the last year, by 24%, on average. Last year, 62% reported an increase, while only 7% saw a decrease in gross annual sales. A total of 25% of respondents said that their gross annual sales in 2020 remained steady from the previous year, compared to 31% who reported a decline in 2019.

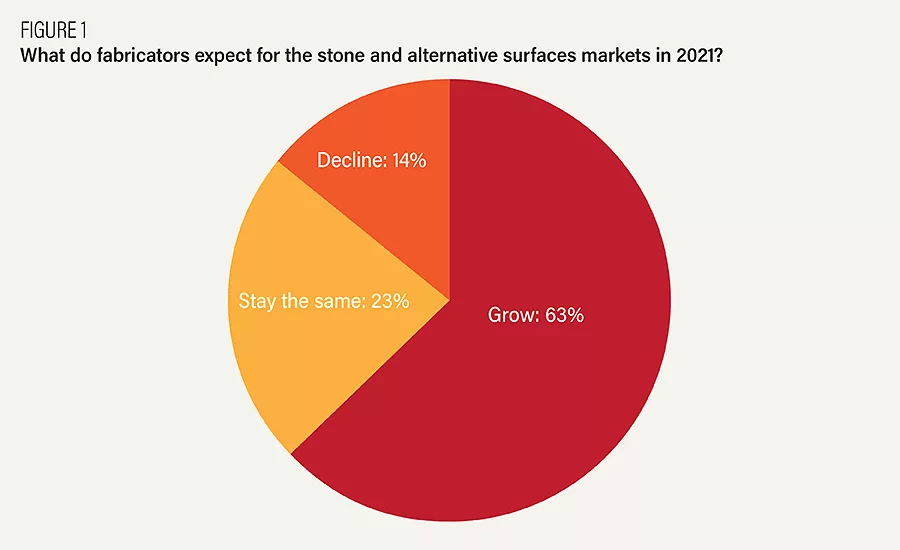

Despite the tumultuous time, more than half (63%) of the fabricators polled in the survey expect sales for the stone and alternative surfaces market to increase in 2021. This percentage is only slightly down from the 67% who expressed optimism about 2020. A total of 23% believe sales will remain the same, while 14% are bracing for a decrease in revenue.

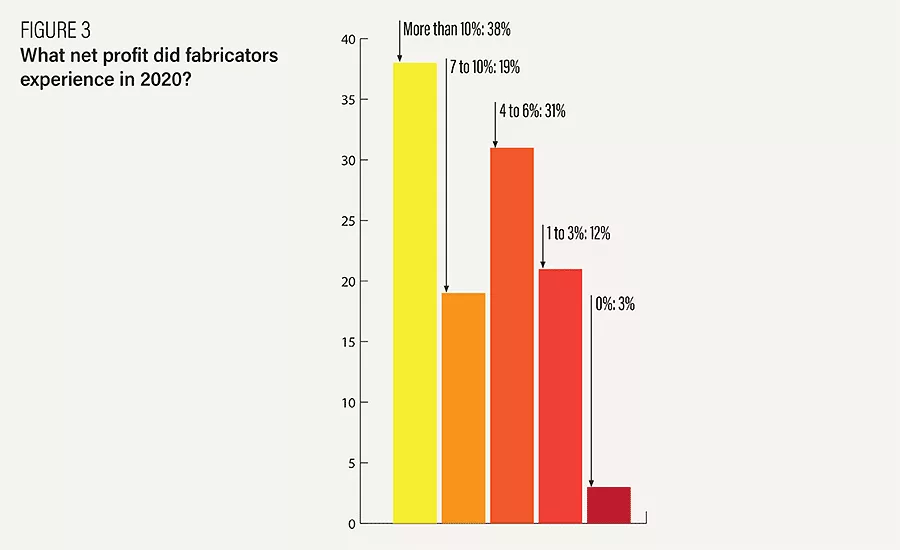

The survey reports 38% of participants experienced a net profit of more than 10% in 2020, not too much of a decrease from last year’s 42%, given the circumstances. Additionally, 19% reported a net profit between 7 to 10% in 2020, compared to 28% in this category the year before. Other results included 31% reporting a 4 to 6% net profit, 12% between 1 to 3% and 3% not experiencing any net profit in 2020.

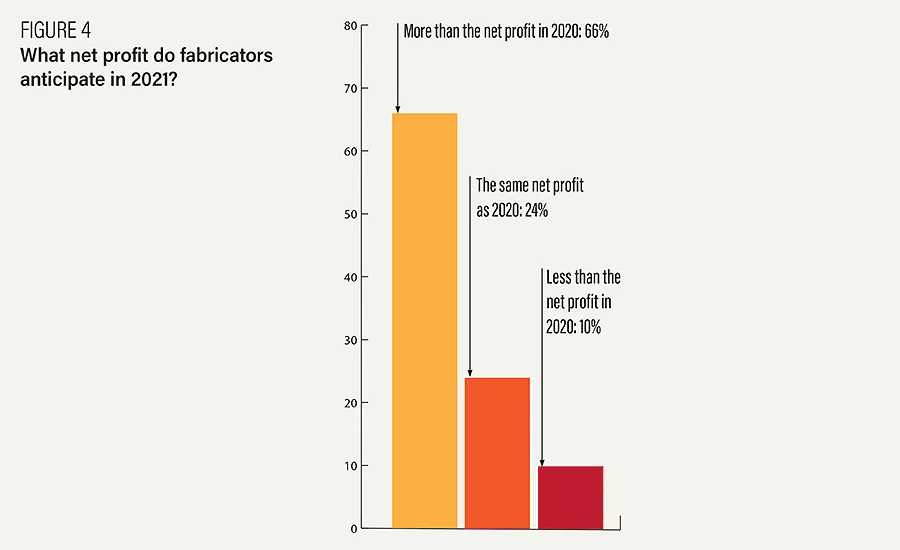

Looking ahead to 2021, the results seem promising. A total of 66% foresee receiving a net profit more than in 2020, 24% expect the same as last year and 10% anticipate a net profit less than 2020.

Impacts of the pandemic

As it has been stated, and experienced first-hand, the COVID-19 pandemic has caused hardships and even crippling effects at times. The majority of respondents agree that employees have played an important role in redefining onsite work space, adjustments to health and safety protocols have been made to ensure employees’ health, customer interaction has changed, employees have exceeded expectations to help the company, and/or employees took the necessary precautions in order to get back to work.

The following are the poll results to a series of questions about working through the pandemic.

- Employees have played an important role in redefining the onsite work space to allow for social distancing: 62% completely agree, while 28% mostly agree, 8% are on the fence and 2% disagree with the statement.

- Many adjustments to health and safety protocols have been made to ensure we keep employees healthy: 67% completely agree, 22% mostly agree, 10% find it debatable and 1% disagree.

- We’ve had to completely change how we interact with customers: 58% completely agree, 27% mostly agree, 10% are on the fence, 4% disagree and 1% completely disagree.

- Employees exceeded our expectations to help the company move forward during this challenging time: 60% completely agree, 24% mostly agree, 9% find it debatable, 6% disagree and 1% completely disagree.

- Employees recognize the threat of COVID-19 and willingly took the necessary precautions to quickly get back to work: 60% completely agree, 21% mostly agree, 16% are on the fence, 3% disagree and 1% completely disagree.

- Most employees are highly concerned about working during the pandemic: 40% completely agree, 35% mostly agree, 12% find it debatable, 9% disagree and 4% completely disagree.

- Many customers have cancelled or delayed projects as a result of the pandemic: 36% completely agree, 33% mostly agree, 12% are on the fence, 11% disagree and 9% completely disagree.

- We’ve made very few modifications to our business and are waiting for the pandemic to end: 23% completely agree, 18% mostly agree, 17% find it debatable, 19% disagree and 24% completely disagree.

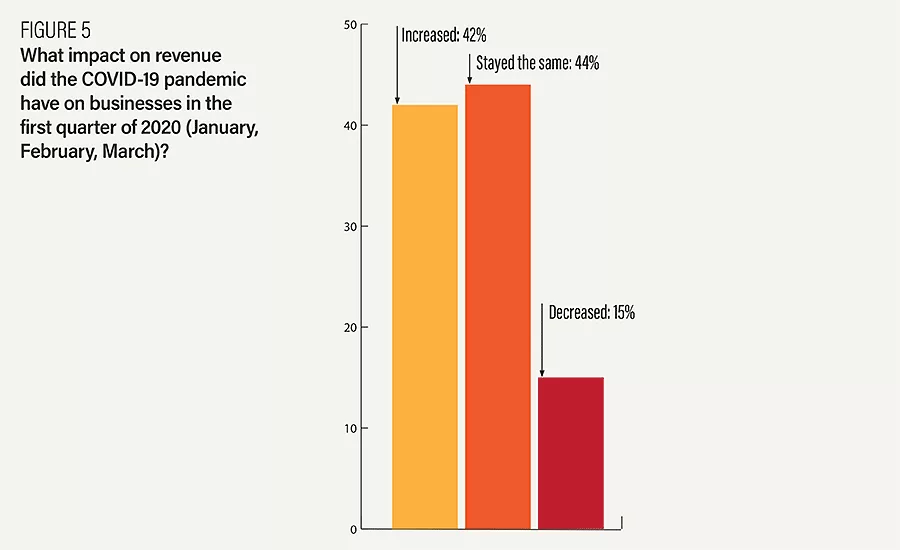

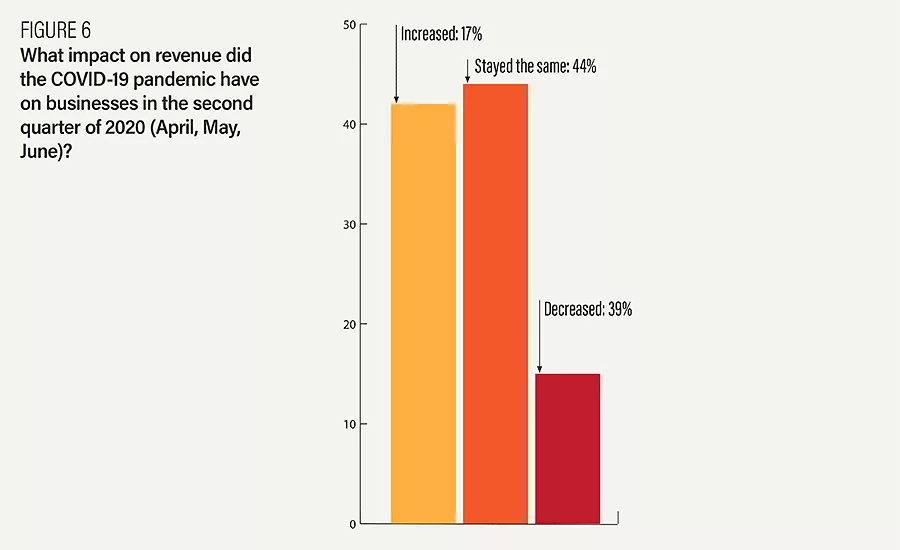

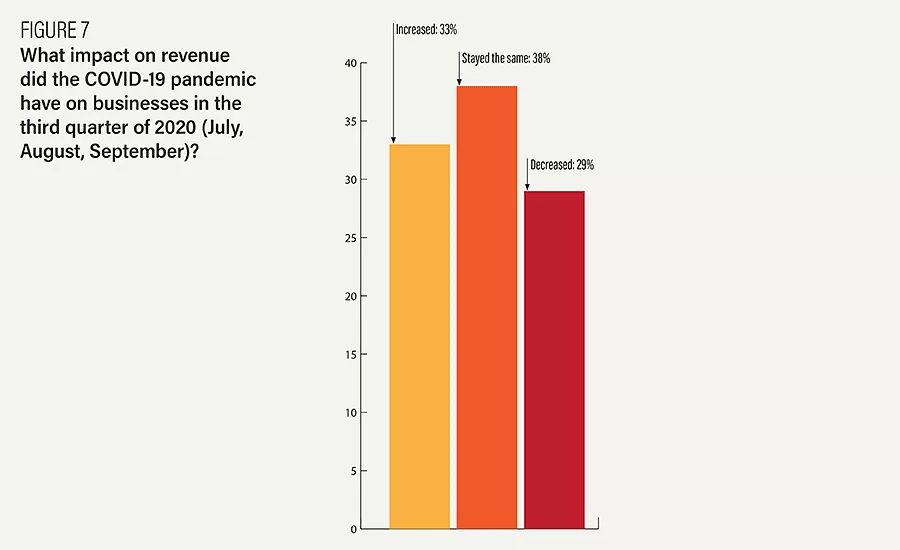

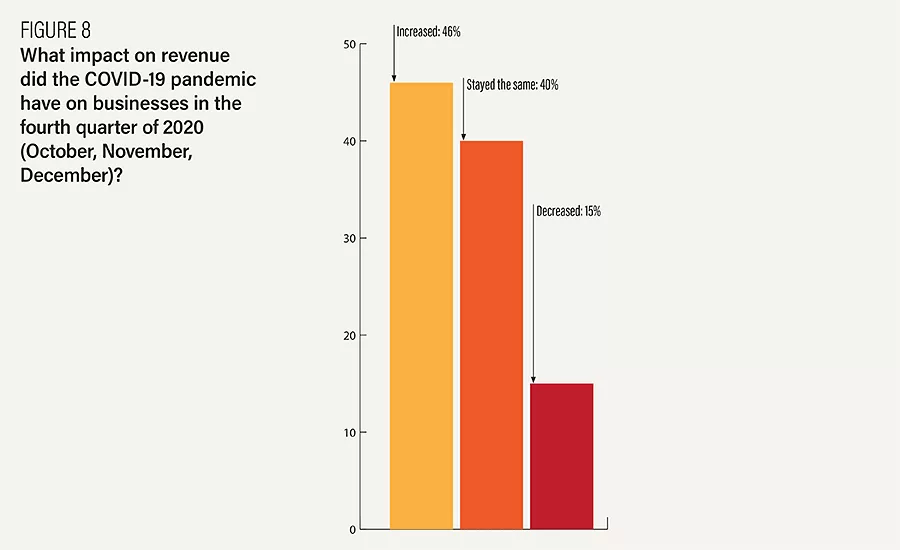

Compared to the second quarter of 2019, revenue in the second quarter of 2020 was down for two-fifths of respondents’ (39%). Respondents were optimistic that the fourth quarter revenues of 2020 would be similar to or greater than that in 2019.

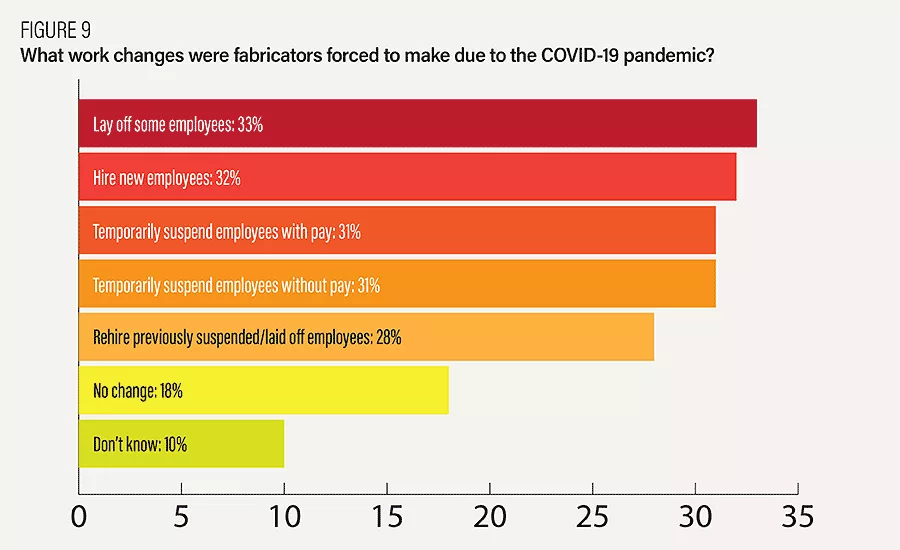

The COVID-19 pandemic also brought changes to the workforce for many. Roughly one-third of respondents indicated that their companies have laid off some employees (33%), hired new employees (32%), temporarily suspended employees with pay (31%), temporarily suspended employees without pay (31%) and rehired previously suspended/laid off employees (28%). On the other hand, a total of 18% stated that they did not make any changes to their workforce.

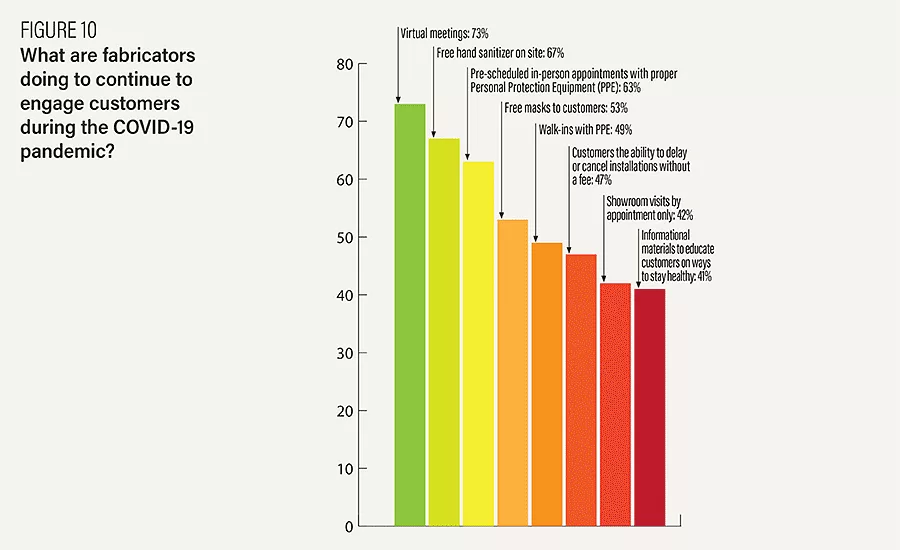

Moreover, the pandemic has also impacted customer and employee engagement. The majority of respondents’ companies are now offering virtual meetings (73%), providing hand sanitizer (67%), scheduling appointments (63%), and/or offering free masks (53%) in order to address customer concerns. In order to keep employees healthy and safe, more than three-quarters of respondents indicated that their companies have increased cleaning/sanitization (79%) and/or are providing PPE (77%). Additionally, 61% mandate daily temperature checks for their employees, 53% require self-reported health checks on a daily basis and 47% are splitting their workforce into shifts to reduce the number of employees onsite.

Capital outlay and business concerns

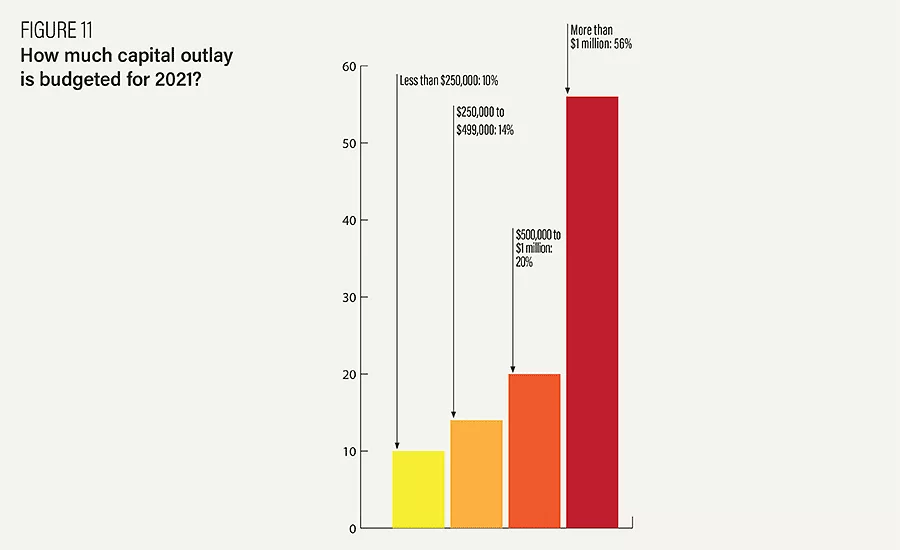

Nearly half of respondents stated their current capital outlay to be between $500,000 and $1 million (46%), while 28% reported it to be more than $1 million. This compares to 26% and 25% in 2019, respectively. When asked to predict their capital outlay for 2020, 56% stated more than $1 million, while 20% stated between $500,000 and $1 million. This compares to 25% and 24% in 2019, respectively.

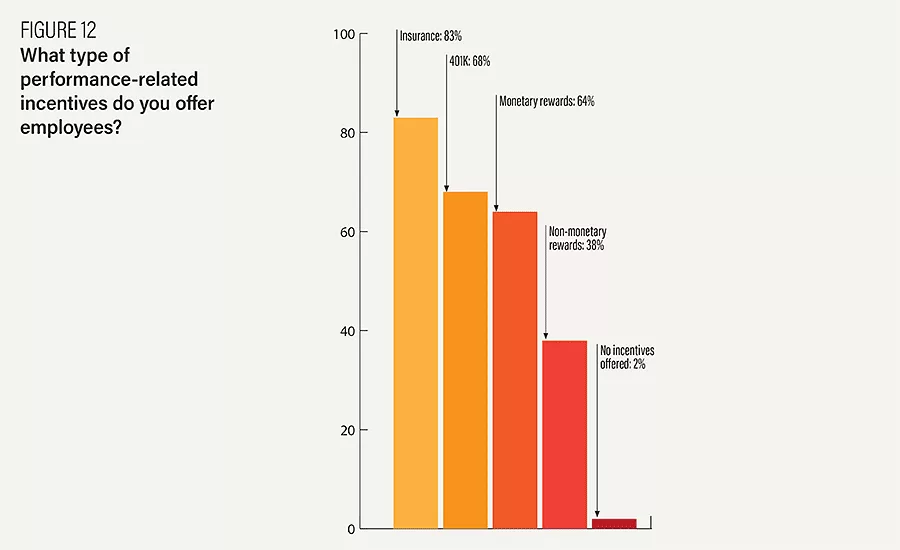

Many of the survey participants invest in their employees to create a sense of company culture and loyalty. A total of 83% offer insurance, compared to 53% in 2019; 68% offer a 401K, compared to 39% in 2019; 64% offer monetary rewards, compared to 58% in 2019; and 38% offer non-monetary rewards such as extra vacation time, compared to 44% in 2019. Only 2% of respondents do not offer their employees incentives, compared to 13% in 2019.

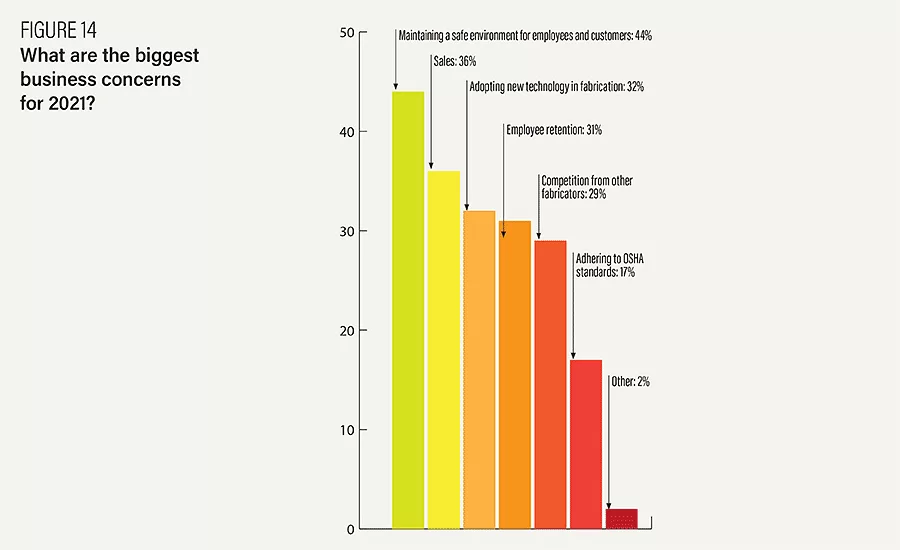

When asked what their primary business concerns are for the coming year, 44% stated maintaining a safe environment for employees and customers, while 36% indicated sales. This is a 5% decrease from the 41% who reported sales were a concern for 2020. A total of 32% are worried about adopting new technology in fabrication, which is similar to the 33% who shared this concern for 2020. Concern over employee retention for 2021 dropped to 31%, an 11% decrease from the 42% who saw this as a problem for 2019. Competition from other fabricators continues to drop. A total of 29% of participants expressed concern for 2021, while 31% did for 2019 and 47% for 2018. Adhering to OSHA standards is top-of-mind for 17% of respondents, down 5% from last year.

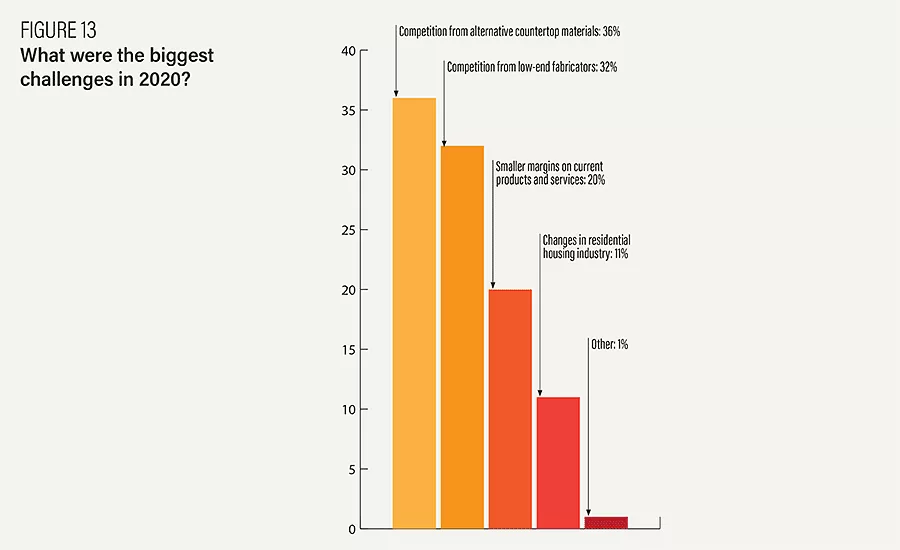

Reflecting on the biggest challenges in 2020, participants reported competition from alternative countertop materials (36%), competition from low-end fabricators (32%), smaller margins on current products and services (20%) and changes in residential housing industry (11%).

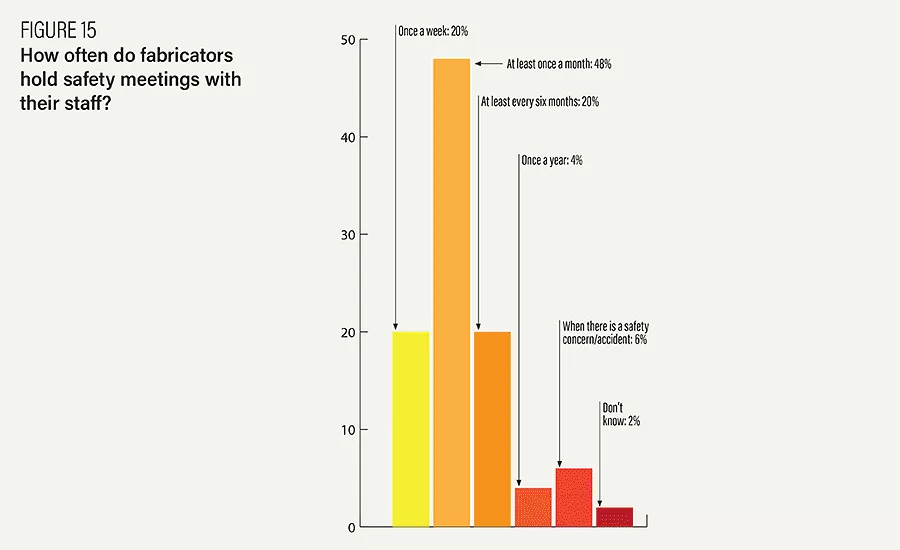

Safety in the shop remains a priority for many fabricators. A total of 20% of those polled hold weekly staff meetings on safety, while 33% did in 2019. Monthly meetings are held among many of the participants (48%, compared to 32% in 2019), while other respondents (20%) hold them at least every six months.

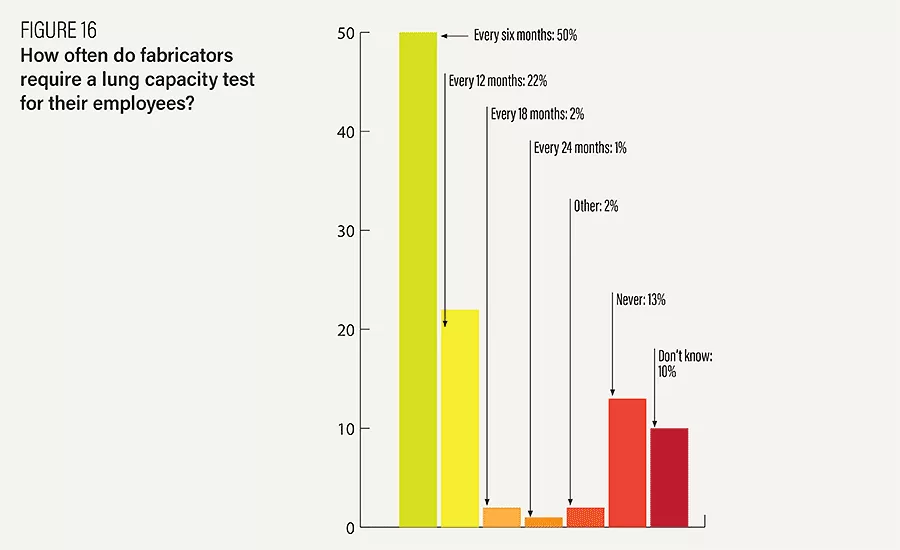

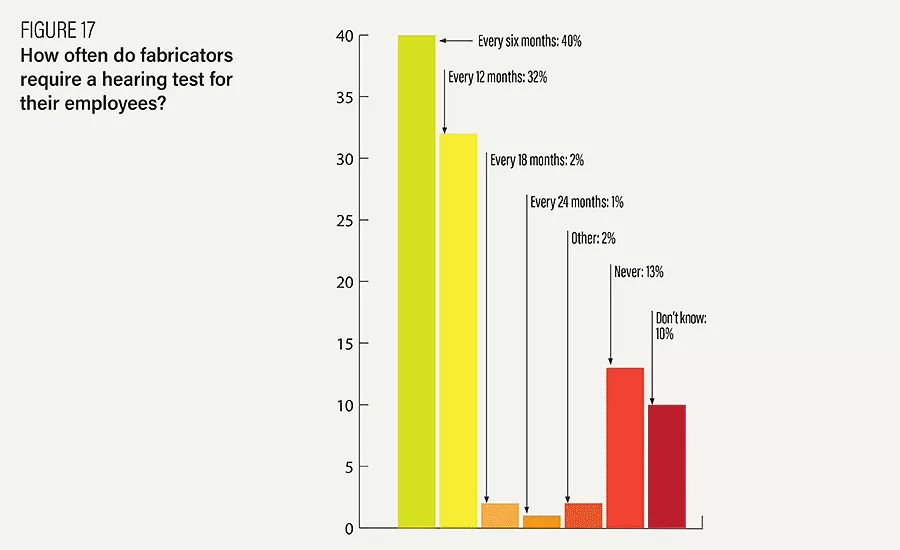

A lung capacity test is required at least once a year for nearly three-quarters of respondents (72%). Hearing tests are also taken seriously, with 72% of respondents requiring them as well.

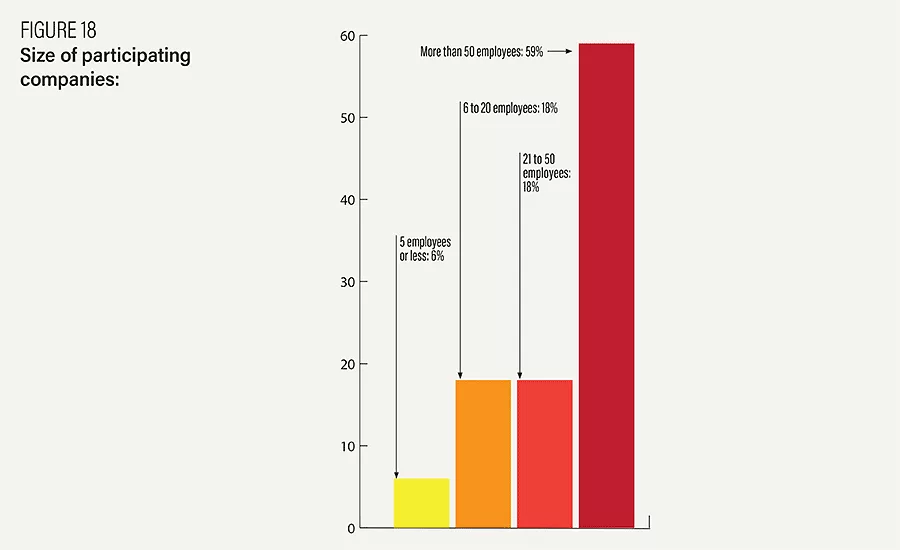

Of those responding to the Stone World fabricator survey, 59% have more than 50 employees, 18% have either a staff of six to 20 employees or 21 to 50 employees, and the remaining 6% have five employees or less. A total of 33% are from the West, 29% from the South, 24% from the Northeast and 14% from the Midwest.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!