A promising forecast for 2020

With more than half of the respondents to Stone World’s annual Purchasing Plan Survey counting on increased sales in the coming year, it appears 2020 is starting off on a high note among fabricators

Overall, the majority of those polled in Stone World’s recent Purchasing Plan Survey, which is conducted by Clear Seas Research Department at BNP Media (Stone World’s parent company), seem optimistic about their businesses in 2020. While investments might not reach as high as last year, there are fabricators who are planning to spend some money. This year’s survey results suggest large machinery and management software are a top priority for many fabricators. We were also happy to see safety ranks high with the majority of respondents, as they hold regular meetings to discuss issues and protocol with their workers and inforce mandatory hearing and lung capacity tests. The following is a detailed account of where the group of polled industry members stand on their predictions and practices for 2020.

2020 forecast

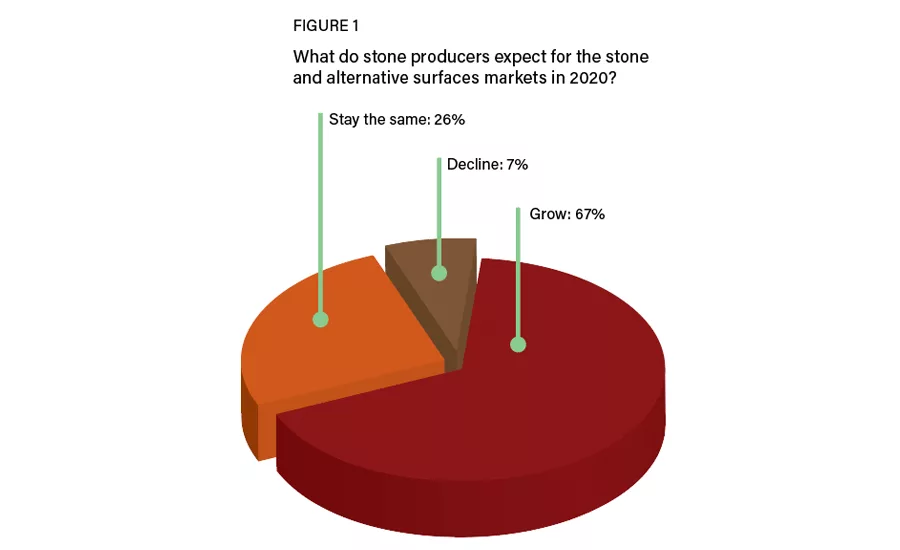

While the majority of participants’ expectations for the coming year are positive, there is a drop in the overall optimism for 2020 compared to last year. While 67% believe sales will increase this year, it is a 15% drop from the 82% that believed sales would increase in 2019. A total of 26% feel sales will remain the same, while 7% foresee a decrease in revenue. The mean average of 19% growth is a 7% decrease from last year’s results, but is equal to the results that were predicted for 2018.

Those fabricators who believe that sales will increase this year, pointed to positive factors in the economy and increased market demand. “There’s general economic growth and full employment in the area,” stated one participant. “Also, there’s an uptick in the construction industry.” Another person polled shared similar sentiments. “Our sales have been increasing month to month,” said the fabricator. “We are seeing a lot of new construction activity in our area that includes stonework. Interest in our products and services has shown substantial increase this year. We expect 2020 to be no different.”

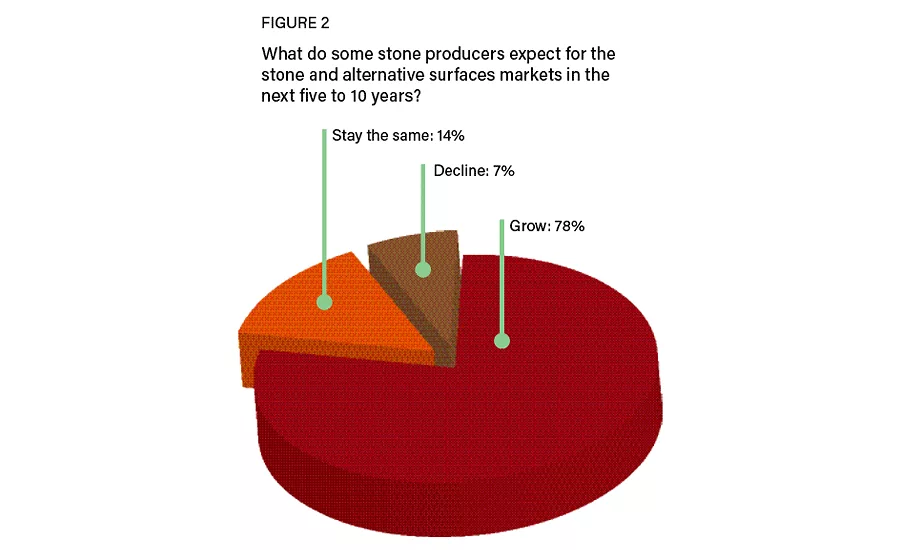

Along these lines, 78% of those participating in the Stone World survey expect business to continue to grow over the next five to 10 years by an average of 20%. This is down from the 82% last year who foresaw the market to continue to grow by 24%. A total of 14% said the stone market will remain stable during the next five to 10 years, and another 7% believe there will be a decline over this period.

Many respondents agree that the stone and alternative surfaces market sales revenues will continue to climb in the future as a result of the increased demand for the products. They also say growth in construction, durability/quality of materials and the growing economy will push sales revenues to grow. “Renovations will make a comeback and new design processes will be needed,” said one fabricator. “Stone is a lasting product and people are more than willing to pay for things that last,” stated another.

Equipment investments

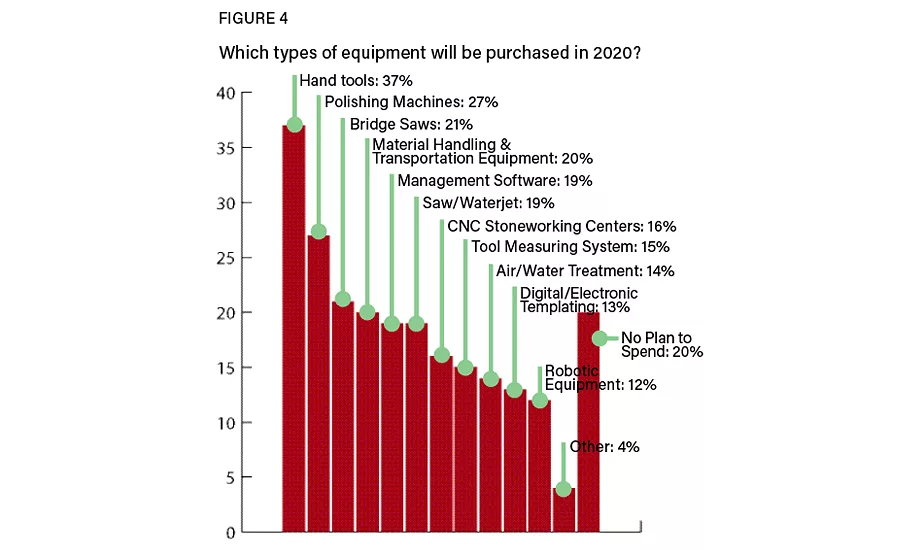

While there are fabricators that plan to invest in technology in 2020, the results indicate spending will be more conservative over last year. Hand tools (37%), followed by polishing machines (27%), are the top two types of equipment to be purchased this year. However, one-in-five respondents (20%) do not plan to purchase any equipment. This is slightly a lesser amount than the 24% who weren’t planning to buy in 2019.

Additional plans for equipment spending include: bridge saws (21%), material handling and transportation equipment (20%), management software (19%), saw/waterjet (19%), CNC stoneworking centers (16%), tooling measuring systems (15%), air/water treatment (14%), digital/electronic templating (13%), robotic equipment (12%) and other equipment not named (4%).

Statistics show the average spending on hand tools in 2020 is expected to be $10,723, which is a drop from the $15,927 fabricators expected to spend in 2019. Those intending to invest in a polishing machine anticipate spending $62,868.

Product quality/reliability emerges as the most important factor when selecting stone-related equipment, with four-in-five respondents (81%) indicating so. Other important points of consideration in 2020 will be availability (63%), price (62%), technical support (58%), brand/company reputation (57%), relationship with manufacturer (46%), customer service/sales rep (46%) and sustainability/environmentally friendly (36%).

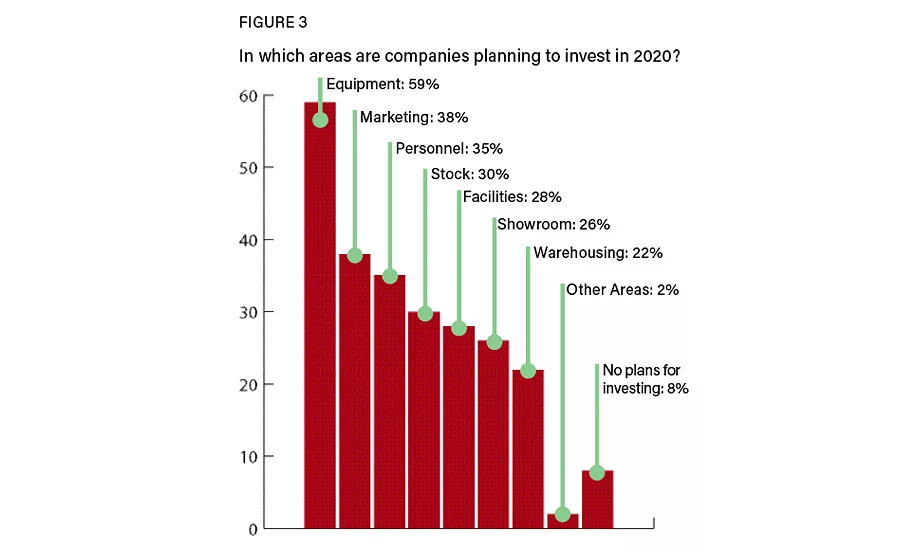

There are fabricators who have budgeted for investments in other areas of their companies as well. While equipment topped the list at 59%, additional spending will be given to marketing (38%), personnel (35%), stock (30%), facilities (28%), showroom (26%), warehousing (22%) and other areas not named (2%). A total of 8% have no plans to make any investments in 2020, which is up 2% for what was forecasted for 2019.

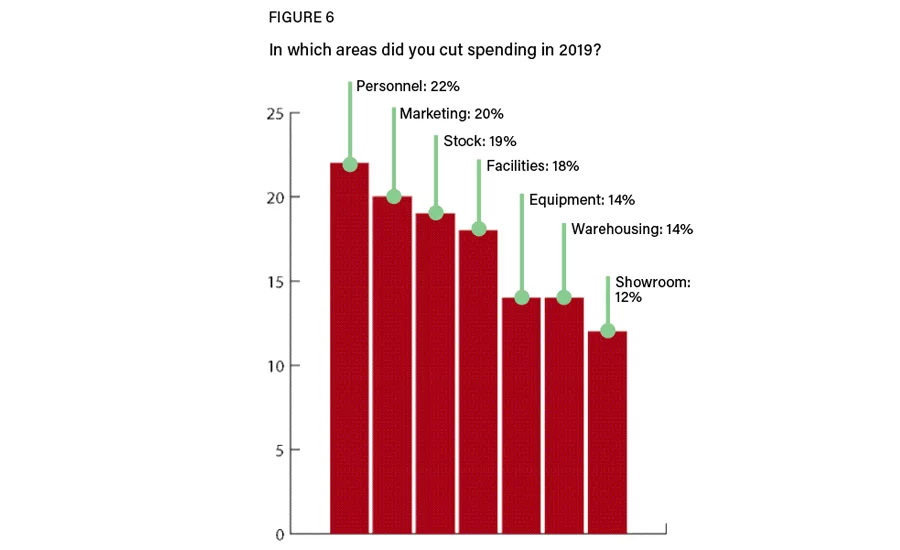

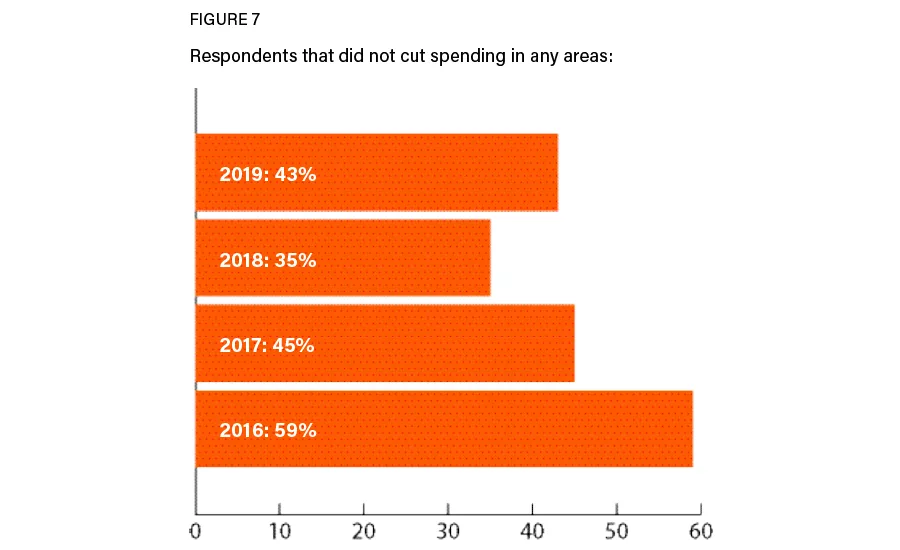

In 2019, there were some who made spending cuts. Personnel was at the top with 22%, followed by marketing (20%), stock (19%), facilities (6%), equipment (14%), warehousing (14%) and showroom (12%). A total of 43% did not cut spending in any areas in 2019, which is up from the 35% who did not make any cuts in 2018.

Business concerns and challenges

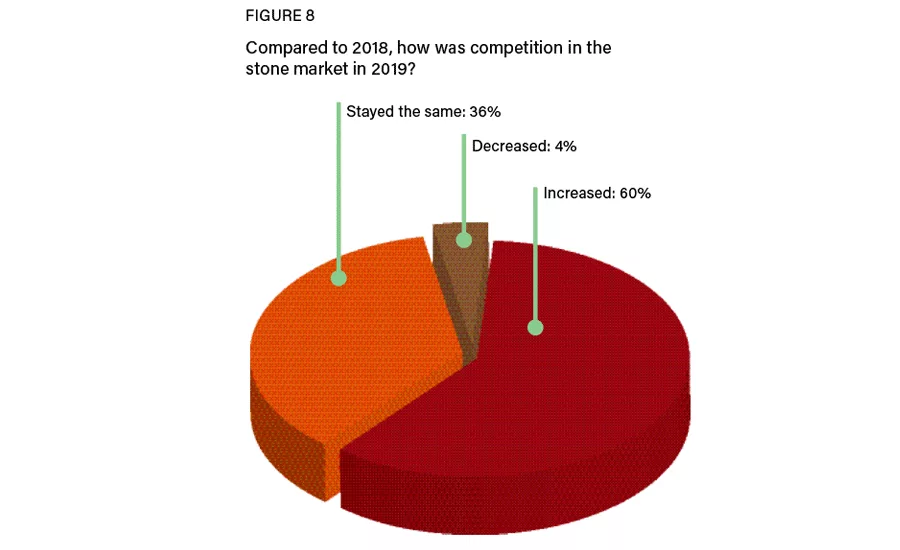

When asked what their primary concerns are for the coming year, two-in-five respondents (42%) said employee retention and/or sales. This is a 7% increase from the 35% who reported this concern for 2019. Additionally, 33% pointed to adopting new technology in fabrication as a challenge, which drastically dropped from the 50% of fabricators who had this concern last year; 31% see competition from other fabricators as a problem (a decrease from the 47% who cited this challenge for 2019) and 22% reported difficulty adhering to OSHA standards, which is up 1% from last year.

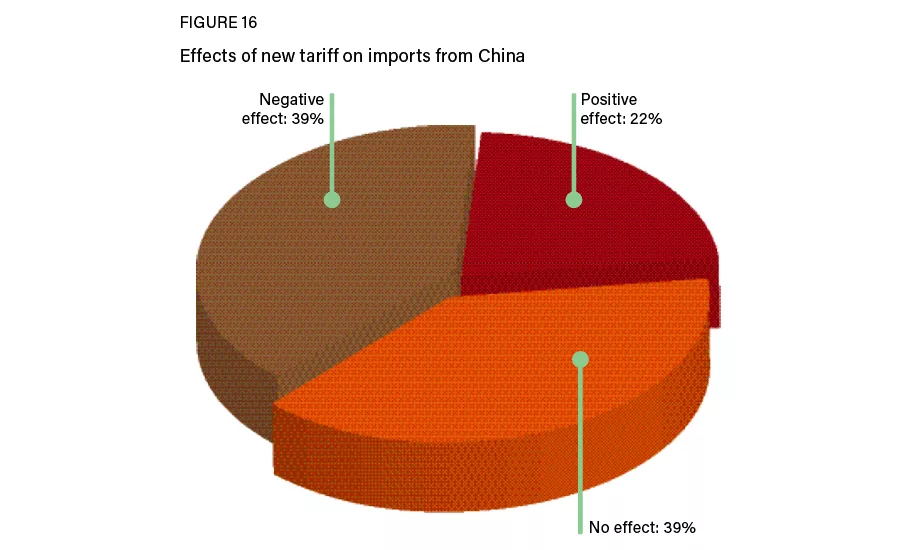

Two-fifths of respondents (39%) report that the new tariff on imports from China has had a negative effect on their quartz production. This is up 7% from those that expressed it was a challenge in 2019. Another 39% reported that the tariff on imports from China has had no impact on their business, which is significantly up from the 18% who shared these sentiments in 2019, and 22% reported the tariff has had a positive effect on their business, which is a large decline from the 50% who reported this last year.

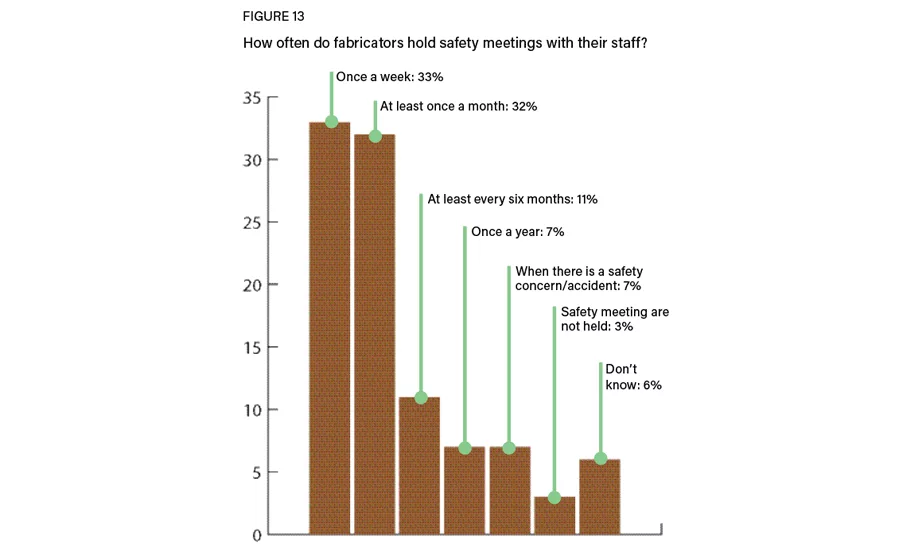

Safety in the shop is a priority for many fabricators. A total of 33% hold weekly staff meetings on safety, while another 32% meet with their staff at least once a month to go over safety issues and protocol. The survey also found that 11% hold safety meetings at least every six months, while 7% hold them once a year. Another 7% only bring their staff together for a safety meeting when there is a specific safety concern/accident, while 3% don’t address safety issues with their shop workers at all. More than half of respondents reported that an OSHA consultant has evaluated their shop in the past three years – two times on average.

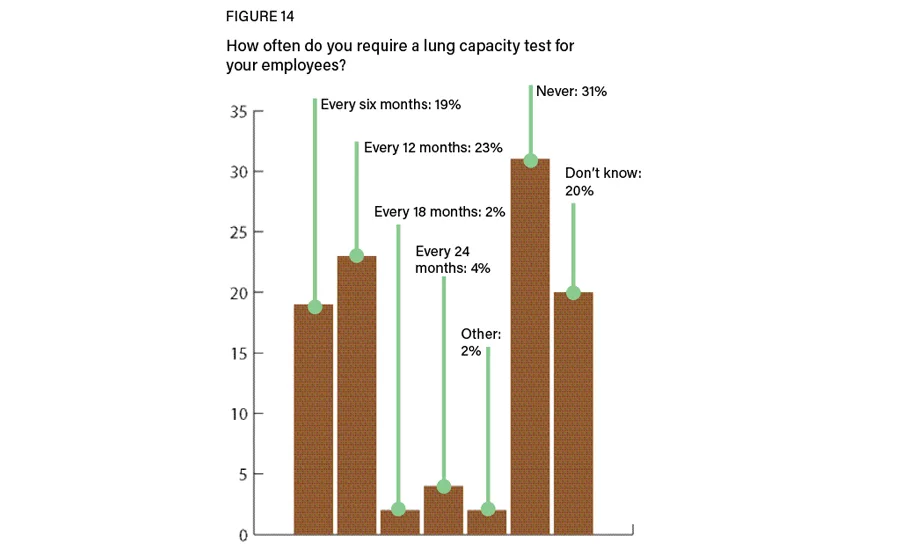

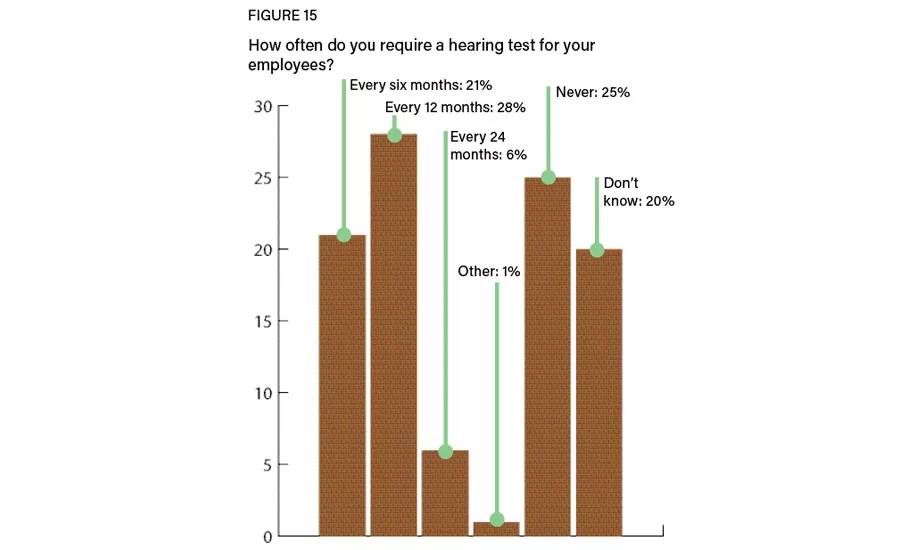

A lung capacity test is required at least once a year for two-in-five respondents, while hearing tests are required for nearly half of respondents at least once a year. However, 20% of respondents do not know how often either test is required, and at least one-quarter reported that these tests are never required.

A look back on 2019

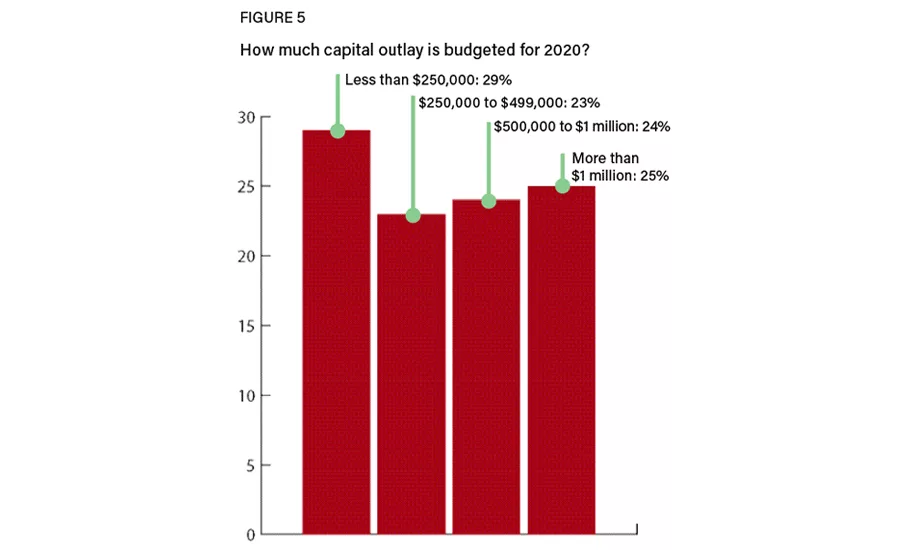

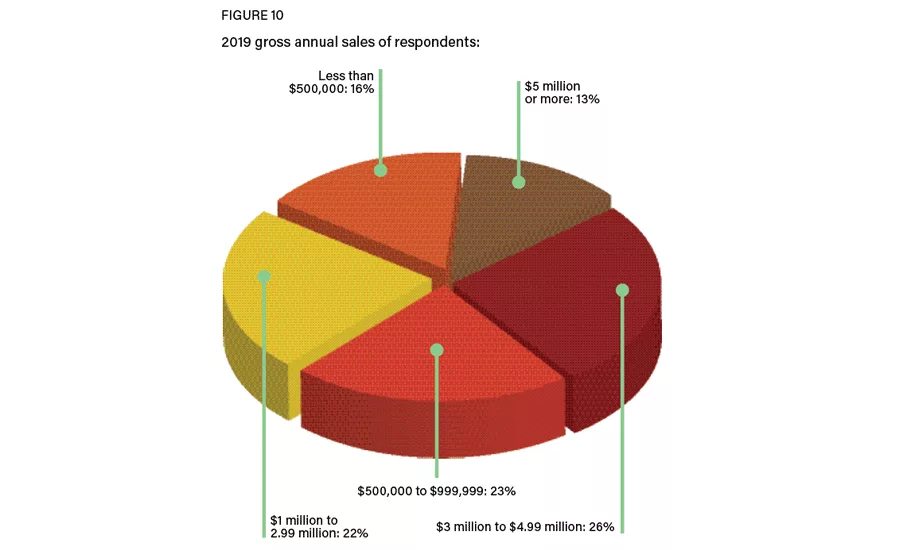

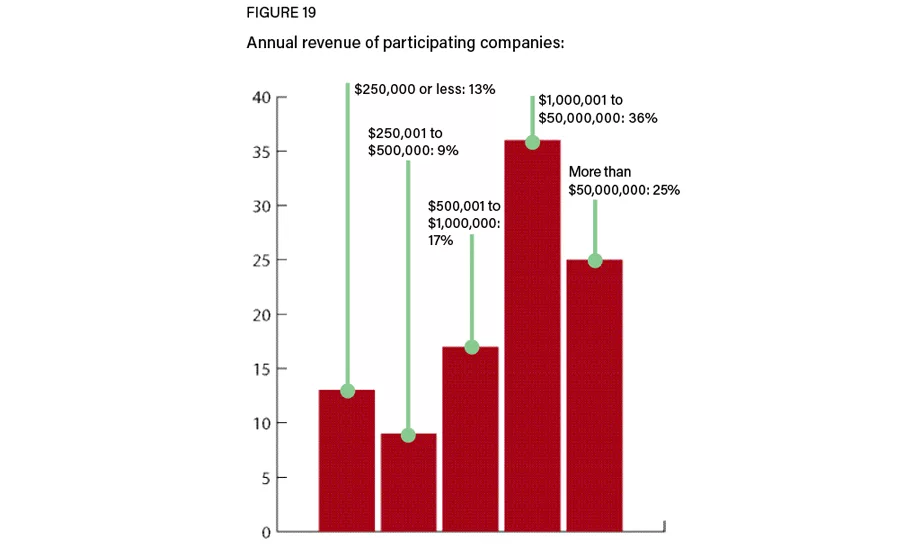

When looking at gross annual sales, 13% of respondents reported that they were between $5 million or more in 2019 (compared to 26% in 2018); 26% were between $3 million and $4.9 million (up from 15% in 2018); 22% made between $1 million and $2.9 million (significantly down from the 41% that had these numbers in 2018); 23% reported annual revenue to be between $500,000 and $999,999 (up 8% from 2018), and 16% said they made $499,999 or less (compared to 3% in 2018).

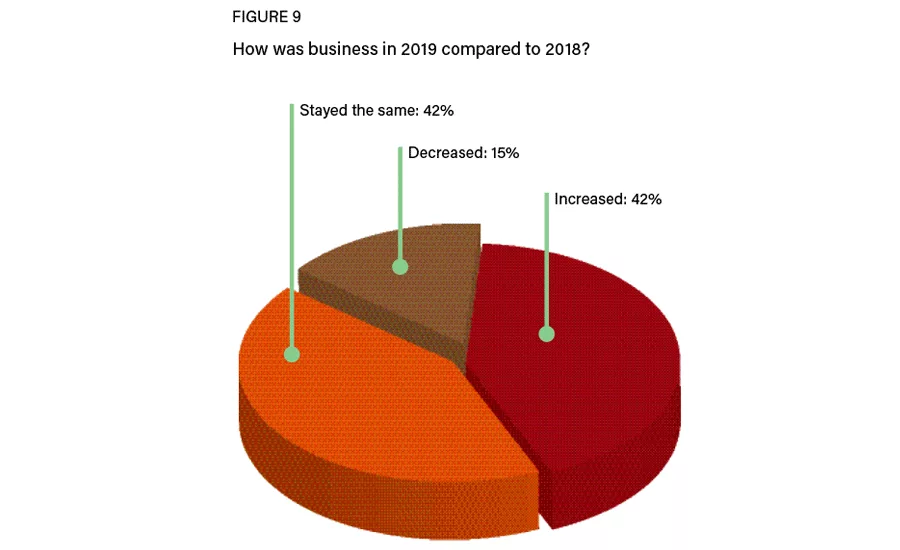

A total of 42% indicated that their companies’ net profit in 2019 was more than 10% — a significant upturn from the 29% who reported this for 2018. The rest of the numbers were as follows: 28% said their net profit was 7 to 10%, 19% said it was between 4 to 6%, 8% said it worked out to 1 to 3% and 3% stated their companies’ net profit was 0%. When asked what they anticipated their companies’ net profit to be in 2020, 52% believe it will be more than the net profit of 2019, 43% said it will stay the same and 5% stated it will be less than the net profit last year.

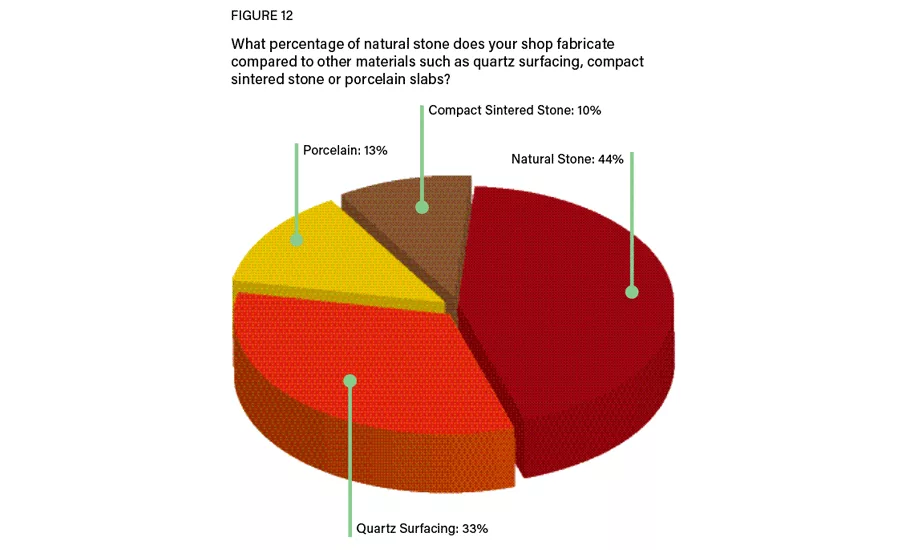

When it comes to material, on average, two-fifths of respondents cut natural stone (44%), followed by one-third who cut quartz surfacing (33%). A total of 13% reported cutting porcelain and 10% fabricating compact sintered stone.

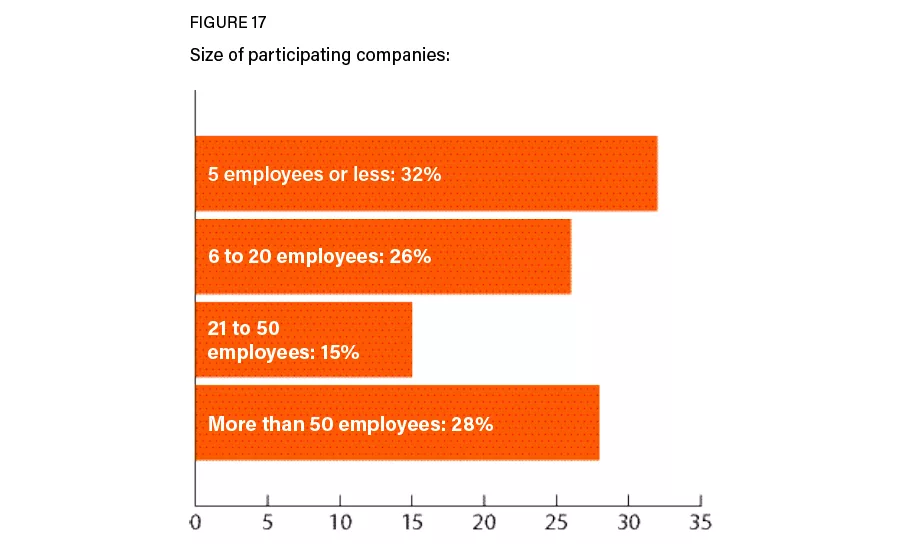

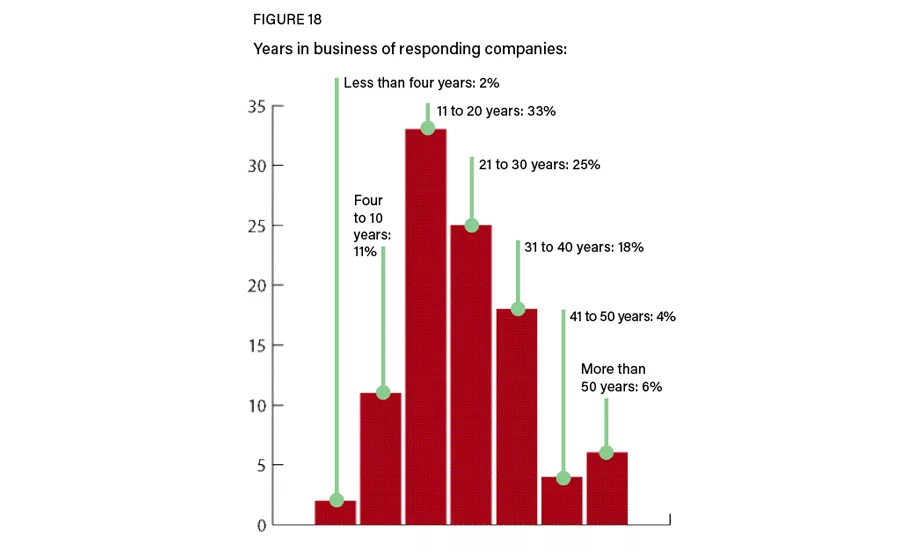

Of those responding to the Stone World fabricator survey, 32% have five employees or less, 26% have a staff of six to 20 employees, 15% have 21 to 50 employees and 28% have more than 50. The majority of those polled (33%) have been in business between 11 and 20 years. Of the respondents, 28% are from the west, 29% from the south, 16% from the Northeast and 27% from the Midwest.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!