Fabricators optimistic for 2011

For many stone fabricators in the U.S., the past few years have been the roughest on record. Not only have they been struggling to withstand an economic recession that has lingered far longer than expected, but they are also facing continued competition from low-cost competitors. Despite all of this, they are generally optimistic that 2011 will be a year of recovery, and this recovery will continue over the long term. Moreover, they are planning to make investments - some of them major - to back up those beliefs.

These are the results of a survey conducted by the Market Research Department at BNP Media (Stone World’s parent company), and it polled fabricators across the U.S., including large and small firms as well as relatively new and well-established companies.

Predictions for 2011

Speaking on the coming year, fabricators seemed to feel that the worst is well behind us. A total of 53% of respondents said the stone market will increase in 2011; 37.4% said it would stay the same; only 9.6% said there would be further declines. This is a fair bit more optimistic than last year, when only 45% expected growth and 15% expected further declines.

Among fabricators calling for growth this year, the majority (65.6%) said that increases would be greater than 6%. Moreover, approximately one out of six fabricators (14.6%) , predicted growth of 11% or more.

When asked why they were optimistic for 2011, fabricators pointed to a general economic recovery and activity in the residential remodeling sector. “Most homeowners are upgrading their homes instead of selling them, and this increases the market for stone remodeling,” stated one fabricator, expressing a sentiment repeated by many survey participants. Another respondent stated: “More people are starting to ease back into spending. Although hesitant, people are starting to spend money.”

A significant percentage of fabricators pointed to their logbooks as a reason for optimism. “There is more market activity,” stated one respondent. “Quote levels are growing, backlogs are growing, and general interest inquiries are growing.” Similar statements were made by a number of other fabricators.

Some fabricators said that customers are resuming projects that were put on hold due to the recession. “Commercial and residential lending standards are thawing, and that will allow for construction to resume on numerous projects that were put on hold as well as for new projects to begin,” stated one respondent.

Long-term optimism

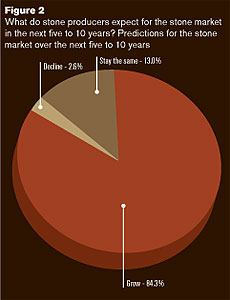

Fabricators have an even more favorable view of the next five to 10 years. According to the Stone World survey, the vast majority of fabricators (84.3%) predicted that the market for stone will increase over the next five to 10 years. Another 13% felt the market would remain stable, and only 2.6% were predicting a decline.

However, even though most fabricators feel the worst is in the past, they feel that the recovery will be gradual. Speaking about the amount of growth to be seen, only 23.7% of fabricators said that increases would be more than 11%. Just under half of the respondents (48.5%) felt the increases would be more in the neighborhood of 6 to 10%.

Once again, fabricators spoke about an overall uptick in consumer spending as reason for long-term optimism. “I believe the market will rebound, and homeowners will continue to invest in upgrading their homes,” stated one respondent, a thought that was echoed by a number of others.

Fabricators also pointed to the amount of houses that were foreclosed on during the recession as a source of new business. “As the economy does finally recover, many of the properties that have been foreclosed on - and other projects that have been put on hold for financial reasons - will start coming through the industry and will temporarily push market numbers up for a period of years,” stated one respondent, with another saying: “Once all the foreclosures are off of the banks’ books, things will start to flow again. It is easy to scare people into not spending, and hard to win them back.”

Respondents to the survey also cited the cyclical nature of the economy, with one stating, “Times roll on a bell curve, and the economy goes up and down. We’ve had down; now it is time for up.”

Once spending does increase on a consistent basis, fabricators seem confident that natural stone will remain at the top of the kitchen countertop market. “As the economy and construction get back to sustained growth, stone will continue to be the preferred surface product,” stated one respondent. Fabricators also cited consumer awareness of natural stone as a key to recovery. “I think education of the public about natural stone - and what to expect from it - will go a long way in building the market. Some regulation in our industry would go a long way, too.”

Additionally, a few respondents spoke about natural stone fitting into the trend towards using green building materials. “In part, [growth will be due] to the green movement, with reasonable cost versus durability and life span of stone.”

Investments during 2011

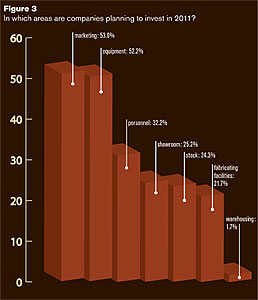

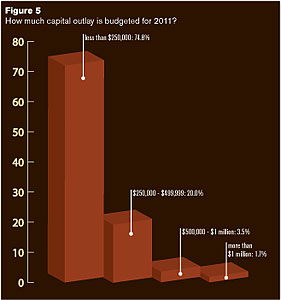

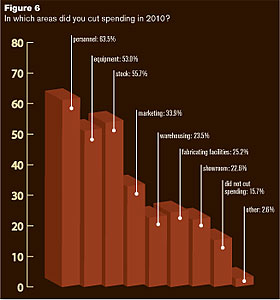

After a year that saw the vast majority of fabricators slashing costs - 84.3% of fabricators polled said they decreased spending in 2010, primarily personnel (63.5%), stock (55.7%) and equipment (53.0%) - fabricators reported that they will be investing back into their businesses this year.

While fabricators still seem hesitant to invest more in stock for 2011 - only 24.3% said they would be doing so - more than half of the survey respondents (52.2%) said they would be spending on equipment this year. They are also planning investments in marketing (53.0%), personnel (32.2%) showrooms (25.2%) and overall facility improvements (21.7%).

For some fabricators, investing in modern stoneworking technology is a strategy to compete against low-cost, low-quality competitors in their area. “The erosion of profitable price points by low end and import fabricators is causing an overall erosion of margins in the industry,” stated one industry respondent. “As a result, fabricators who do not invest in technology and rely solely on shop personnel as their assets will not be able to compete in the market and are at risk of elimination.”

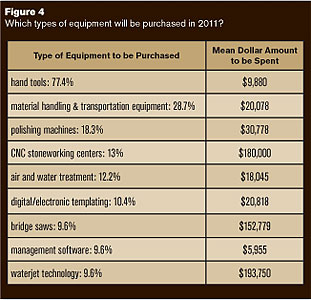

Speaking on specific equipment choices, hand tools were once again mentioned by most fabricators(77.4%), and they expect to spend a mean total of $8,800 in this area.

In terms of larger investments, the percentage of fabricators planning to purchase major machines is on the smaller side, but still significant when considering the amount of money they expect to spend. Of note, more than one in eight fabricators (13%) said they would be purchasing a CNC during 2011 - with a mean value of $200,000. An even higher mean value was placed on waterjet technology, with just under one out of 10 fabricators (9.6%) expecting to spend $193,750 on this equipment this coming year.

As the technology level for bridge sawing equipment increases, so does the mean value that fabricators expect to spend for this machinery, with 9.6% of respondents planning to invest $152,779 in this sector.

With an eye on shop safety, 28.7% of respondents said they would be investing in material handling technology this year, with a mean value of $20,000. Meanwhile, a significant number of shops are adding to their eco-friendly practices by investing in air/water treatment systems, with a mean value of $18,045 for this technology.

Other notable investment plans include polishers, with a total of 18.3% planning to spend a mean value of $30,700; and digital/electronic templating systems, with 10.4% expecting to spend $20,800.

Reflecting back on 2010

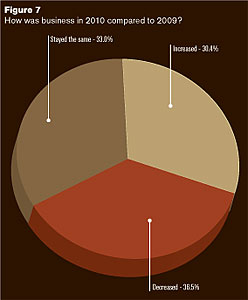

In addition to asking about their future expectations, the Stone World survey asked fabricators to compare their business levels for 2010 to 2009. Responses to this question this year were much more positive than 12 months prior. According to the survey, 36.5% of fabricators saw their business decline during 2010 (a year ago, 68% said they saw a 12-month decline). Meanwhile, 33.0% said that business held steady, and 30.4% said that business improved during 2010. For comparison, only 19% of those polled a year ago said that business increased for the year.

Also encouraging, the fabricators that said business increased said that the gains were significant. A total of 17.1% of fabricators said that growth was more than 20%, and another 20.0% of respondents said that growth was 11% to 20% .

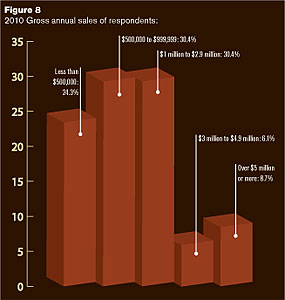

Overall, the bulk of stone fabricators who participated in the survey (85.1%) saw less than $3 million in annual sales. A total of 24.3% reported sales of under $500,000; 30.4% said sales ranged from $500,000 to $1 million; another 30.4% reported sales of $1 million to $2.9 million; 6.1% recorded sales of $3 million to $4. 9million; and 8.7% had a sales total of more than $5 million.

When asked to compare today’s business climate to that of 12 months ago, 40.8% said that conditions were better, 26.1% said they were worse, and 33.0% said they were about the same.

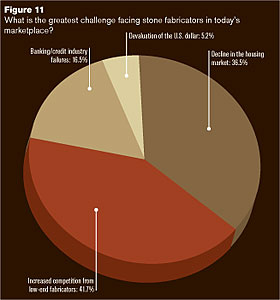

Speaking on the greatest challenges in today’s marketplace, competition from low-end fabricators was cited by more respondents (41%) than any other category, including the decline in the housing market (36.5%), banding/credit industry failures (16.5%) and the devaluation of U.S. currency (5.2%). (See “Lowball competitors seen as greatest threat to U.S. fabrication industry” for fabricator comments on the subject.)

Survey demographics

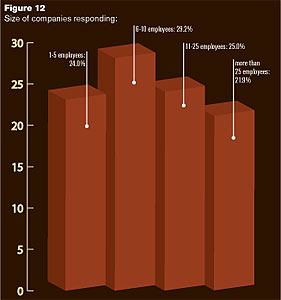

Remaining consistent with our industry makeup, respondents to the Stone World fabricator survey were relatively small in size - although they averaged somewhat higher than in recent years. A total of 24.0% of respondents had one to five employees; 29.2% had six to 10 employees; 25.0% had 11 to 25 employees; and 21.9% had more than 25 employees.

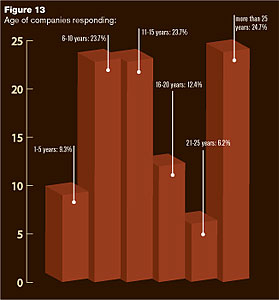

Looking at the amount of time that the survey respondents were in business, fabricators cited a broad range of experience levels, although there were less relatively new companies than in past surveys. A total of 24.7% said they were in business for more than 25 years; 18.6% have 16 to 25 years of experience; 47.4% have 6 to 15 years of experience; and 9.3% have five years of experience or less.

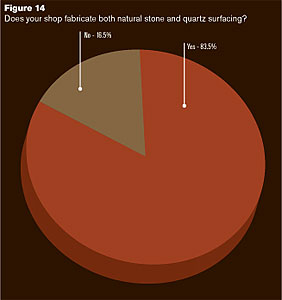

Also of note, most fabricators (83.5%) reported that they are fabricating both natural stone and quartz surfacing products, up from 73% a year ago.

Lowball competitors seen as greatest threat to U.S. fabrication industry

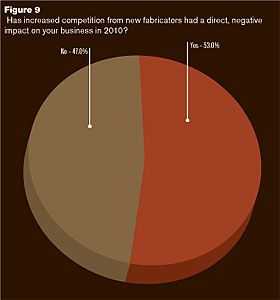

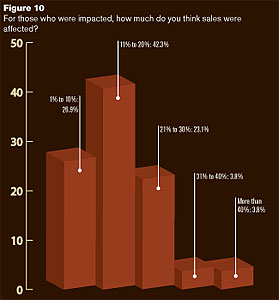

More than ever before, fabricators who participated in this year’s Stone World fabrication market survey cited lowball competitors as a very real threat to their business. According to the survey, more than half of the fabricators polled (53.0%) said that low-cost competitors had a direct, negative impact on their business during 2010.

These impacts were significant, with 42.3% saying that they lost 11 to 20% of their business volume. Another 23.1% said they lost 21 to 30% of their business, and 7.6% lost more than 30% of their business due to this ever-increasing problem.

When offering their candid open-ended responses to the Stone World survey, the amount of fabricators citing low-ball “hacks” was too great to ignore. These responses included the following statements:

• “In my opinion, this business is no longer a custom craft. Its more about Big Box volume, not to mention the fact that every guy with a Skilsaw and a set of polishing pads is now a ‘fabrication shop.’ The industry is flooded, and customers are shopping price rather than quality and service. Times have changed and I feel the medium to small shops will suffer at the hands of fly-by-night shops and mass production.”

• “The worst are the fly-by-night fabricators selling at impossible pricing and doing bad work. Customers’ expectation for a ‘good deal’ have kept pricing suppressed, and I do not see the recovery.”

• “The stone fabricating market has been flooded with (too often incompetent) shops. Though there is more work getting done, it is being spread among the numerous shops, making it seem like there is no growth in the market.”

• “There are several small companies with no overhead and no insurance out bidding very low pricing for granite. It is very difficult for shops like mine to compete, and I think this will result in several mid-size shops closing. Then there will only be the super large shops and the hacks.”

• “We need to get rid of all the small shops that are not insured and don’t pay taxes.”

A number of fabricators were more optimistic, as they felt the lowball fabrication shops will ultimately fail as the economy improves.

• “The garage shops will eventually fail; the superstores will enhance the consumer mentality; and the dedicated mom-and-pop shops will survive. This will even out the playing ground. The ‘man-made’ surfaces will go back to natural material, as they always have.”

• “The shops that thought they could cut prices and survive will be gone.”

• “Once the hack shops fail, maybe we can become a better industry.”

• “There has been an increase in lowballing competition. Due to the quality of their work, I see many of these companies disappearing from the market.”

Some fabricators suggested that the industry needs to unite to offset the influx of lowball competitors:

• “The industry itself [should] pull together to create a loyal atmosphere, rather than a back-stabbing atmosphere. The consumer is driving the pricing, and the industry is not protecting themselves from the backlash of this. Hence, [we have] low profits and illegal activity.”

• Hopefully, there will be a way for all companies to play by the same rules (taxes, insurance, OSHA compliance. That will weed out the illegals and lowballers. I believe all these back-door fabrication shops are going to be pushed out.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!