Who likes paying taxes?

Author: Mark Lindell, Park Industries® Sales Consultant

Co-Author: Rachel Scheck, Park Industries® Communications Specialist

As business is thriving, re-investment decisions must be made. These decisions should be considered with the anticipated future profits in mind. If your company is doing well and seeing profits, the choice is yours on how to utilize those profits. Profits may be spent, re-invested in the company, or a large portion may be spent on taxes. Few look forward to tax season. What if there was a way to decrease taxes while investing in the growth and value of your business?

Investing in equipment for your business is investing in your future profitability. The value of knowing your profitability projections will allow you to make the choice between saving the profits or investing in technology and taking advantage of tax benefits. When deciding where to invest, it is important to understand how you would like your business to grow and allocate with the projected company growth in mind. Your business will benefit from a serious assessment and strategic planning for future profitability.

Section 179

Tax incentives are created so that companies can invest in the future of their business. Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment financed during the tax year. If you buy, or lease, a piece of equipment that qualifies, you can deduct the full purchase price from your gross income. With a more efficient shop process, the company will grow, the value of your company will increase, all while having a positive impact on the U.S. economy.

Not only will the equipment help your shop run more efficiently, but the investment will reduce your tax dollars spent. The 2018 deduction limit is $1,000,000 with equipment that is purchased and put into service by the end of the day, December 31, 2018. To take the deduction for tax year 2018, the equipment must be financed or purchased and put into service between January 1, 2018 and December 31, 2018. When companies have the added benefit of a lower taxable dollar amount, purchasing additional equipment becomes more feasible. In fact, electing the Section 179 deduction allows you to use any portion of it in the current tax year or any future tax years.

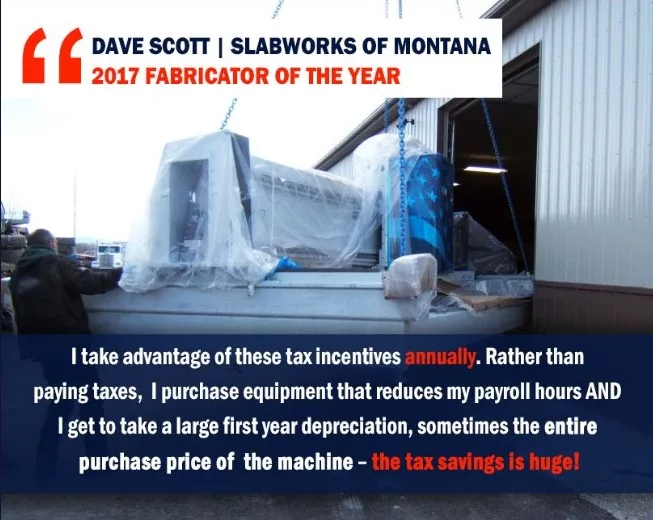

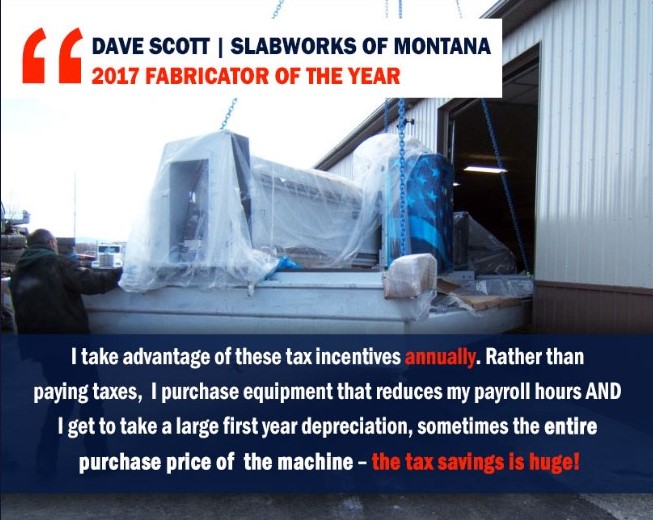

There is a spending cap on equipment purchases before the Section 179 Deduction available to your company begins to be reduced on a dollar for dollar basis. The maximum amount that can be spent on equipment is $2,500,000 for 2018. This spending cap makes Section 179 a true “small business tax incentive”. This tax incentive is in place to allow small to medium sized businesses to grow. Dave Scott, owner of Slabworks of Montana, shares, “I take advantage of these tax incentives annually. Rather than paying taxes, I purchase equipment that reduces my payroll hours AND I get to take a large first year depreciation, sometimes the entire purchase price of the machine – the tax savings is huge!”

Bonus Depreciation

For 2018, companies are able to write off 100% of a machine acquisition. Unlike Section 179 that is dedicated to small businesses, the bonus depreciation can be used in any size business. There is no limitation on how much equipment may be expensed through bonus depreciation. Bonus depreciation is generally taken after the Section 179 spending cap is reached.

Invest in the Future

Your tax advisor will have the ability to provide more insight and details about these enhanced programs. Consult with a tax advisor to learn if you can take advantage of these great tax benefits. Financial decisions must make sense for the short and long-term growth of your company. Tax season will be here shortly. Plan ahead to lower your taxes while investing in the future of your business.

Mark Lindell

Park Industries® Sales Consultant for 15 years.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!